Closing Costs Explained: What Are Closing Costs and How Much Are They?

Budgeting for a home purchase is more than just accounting for your down payment. As a buyer, you’ll also be responsible for a range of fees that cover services and ensure a smooth transaction. Some fees are related to the property itself, while others are required to close and fund your loan.

Note, that if you’re selling, most of your closing costs are related to real estate agent commissions, though the buyer may ask you to cover some of their closing costs as part of the negotiation.

What are closing costs?

Closing costs are fees associated with your home purchase. Some are paid to your lender, and others to third parties such as appraisal, inspection, and title companies, in order to finalize and fund your loan. There are various types of closing costs, with most being paid by the buyer, but some being paid by the seller.

How much are closing costs?

Buyer closing costs are usually between 2% to 5% of the home’s purchase price. For example, if the home costs $300,000, you might pay between $6,000 and $15,000 in closing costs.

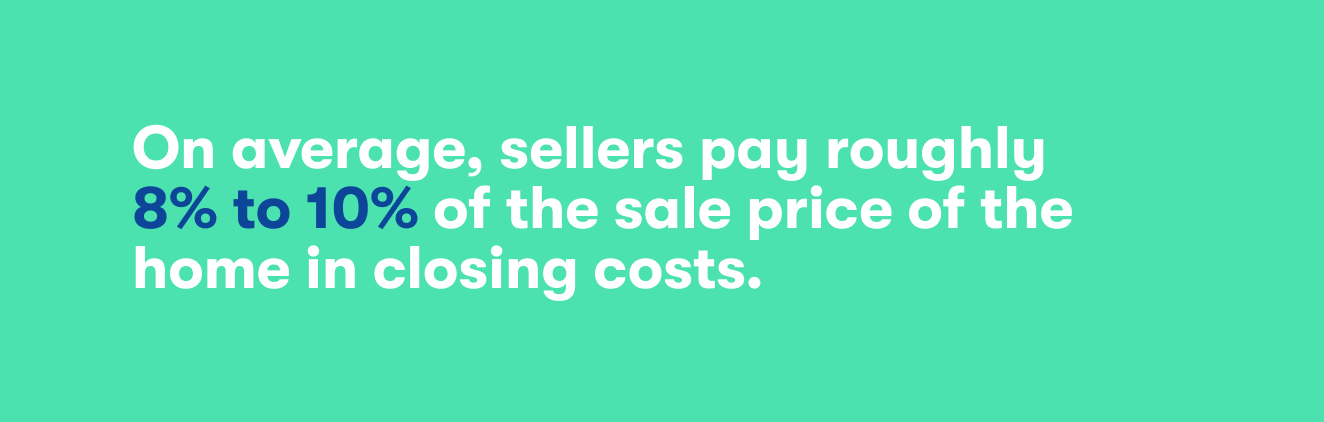

Seller closing costs are typically higher. On average, sellers pay roughly 8% to 10% of the sale price of the home in closing costs — the majority of this cost is made up by agent commissions. On a $300,000 home, that’s between $24,000 and $30,000.

A lot of factors impact how much you’ll pay in closing costs. For buyers, it depends on your loan program, size of loan and individual lender practices. For sellers, it comes down to what you’ve negotiated in terms of concessions and agent commission.

When are closing costs due?

Most closing costs are due on the day of closing, which is the point in time when the title of the property is transferred from the seller to the buyer. Money is typically wired to the receiving parties upon closing, or the buyer will bring a cashier’s check to the closing appointment.

However, there are some closing costs paid before closing day, such as inspections, certifications or land surveys. Home inspections are usually completed within a week of your offer being accepted and are paid for at the time of service. Not all deals require an inspection. It’s usually up to the buyer if they want to add an inspection contingency.

If you are getting a flood zone certification or land survey, you’ll also pay for these at the time of service, though sometimes the cost is shared with the seller.

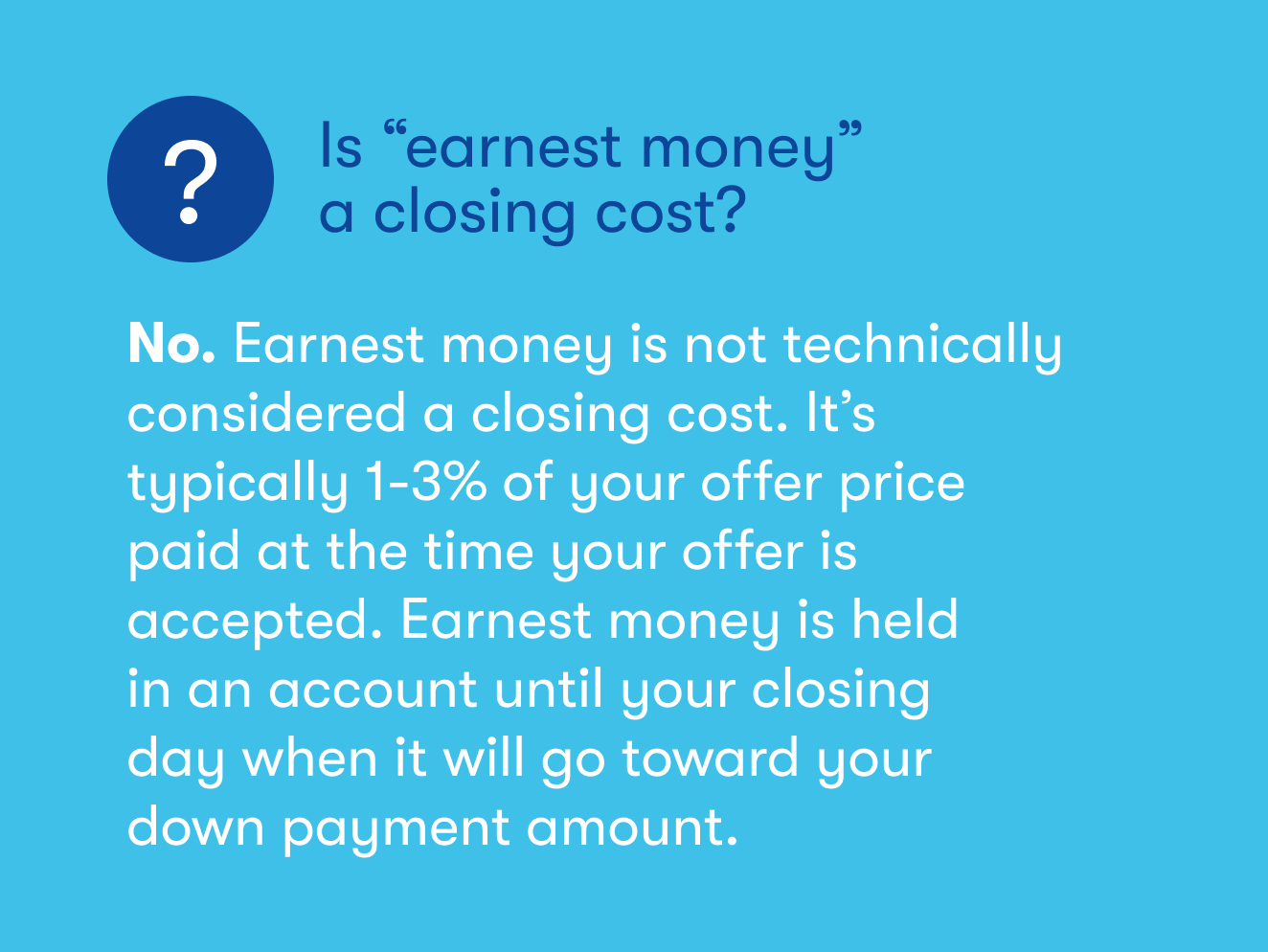

Note: Earnest money is not technically considered a closing cost (nor does it factor into a buyer’s 2% to 5% range), but it plays an important role in your total payment on closing day. It’s typical to make an earnest money deposit when you put an offer in on a home. The average amount ranges between 1% to 3% of the offer price and it’s deposited into a third-party account to show the seller that you’re a serious buyer. It’s held there until closing day when it is applied to your down payment amount.

Closing costs for buyers

Buyer closing costs are a combination of one-time fees and the initial installments of recurring costs you’ll pay alongside your mortgage every month. An example of a recurring cost is your homeowners insurance premium. You’ll likely pay your first year’s premium at closing. In future years, it will be paid either out of pocket or via an escrow account you add funds to every month.

Note that every lender and closing agent bundles closing costs differently. For example, yours may bundle fees like recording fees, courier fees and notary fees into one line item called ‘administrative fees.’

Here’s a quick breakdown of homebuyer closing costs.

One-time fees

- Appraisal fee

- Application fee

- Home inspection fee (plus optional reinspection if the seller makes improvements during the transaction)

- Credit report and credit supplement fees

- Mortgage origination fee

- Lender’s policy title insurance (plus optional owner’s policy title insurance)

- Escrow fee

- Closing attorney fee (in some states)

- Courier fee

- Bank processing fee

- Recording fee

- Notary fee

- Loan discount points

- Homeowners association transfer fees

Recurring fees

- Homeowners insurance

- Property taxes and tax servicing fees (including a prepaid lump sum)

- Mortgage insurance for down payments worth less than 20% of the purchase price (MIP/PMI)

- Flood certification fee (in some areas)

What are the closing costs for cash buyers?

Cash buyers are still required to pay for things like notary fees, property taxes, recording fees, and other local, county and state fees. Unlike a buyer who is using financing, cash buyers won’t have to pay any mortgage-related fees. But most cash buyers still opt to pay for things like appraisals, inspections, and owner’s title insurance.

Closing costs for sellers

Sellers usually pay buyer and listing real estate agent commissions, transfer fees and their own real estate attorney costs. Local rules vary by location, however, and many items can be negotiated by contract.

Here’s a list of the most common closing costs for sellers.

- Agent commission (both seller’s and buyer’s agents)

- Transfer tax

- Title insurance

- Escrow and closing fees

- Prorated property taxes

- HOA fees

- Credits toward closing costs

- Attorney’s fees

How to estimate closing costs

The best way to estimate your closing costs is to review the Loan Estimate provided to you by your lender during the loan application process. If you’re not ready to apply for a loan but want to get a feel for how much you can afford, check out Zillow’s affordability calculator. You can also simply multiply a home’s sale price by 2% to get your minimum closing cost amount or 5% to get the high end of your potential closing costs.

Closing cost estimates fluctuate

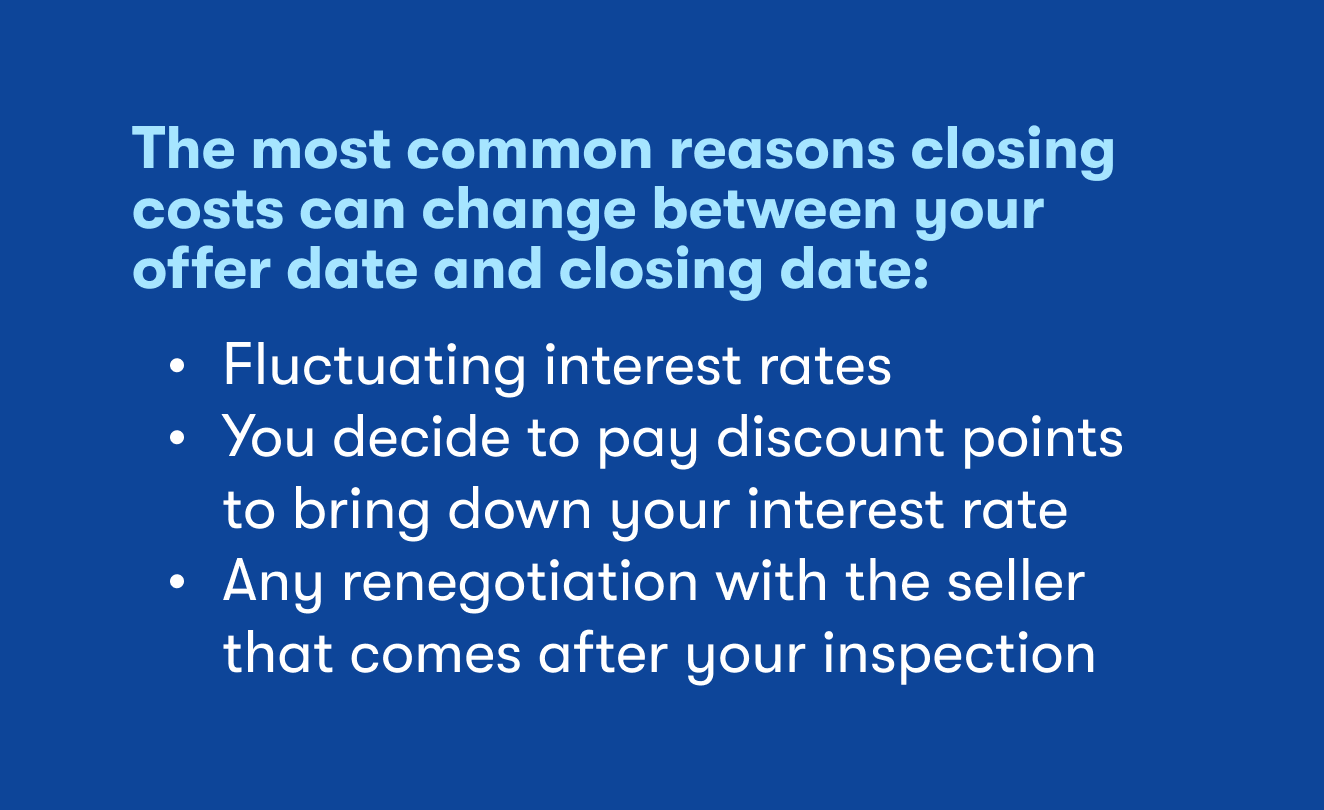

Keep in mind that individual line items may change during the course of the transaction, up until your closing date, since many of the early figures are simply best estimates. The most common changes are related to interest rates fluctuating, deciding to pay discount points to bring down your interest rate or any renegotiation with the seller that comes after your inspection.

If significant changes happen along the way, you’ll receive a revised Loan Estimate.

At least three days before your closing, you’ll receive a Closing Disclosure Statement from your lender. Be sure to take the time to compare this final statement with your Loan Estimate, and ask your lender to explain any line items that have changed. There are limits to the amount that fees can increase between the time you receive your Loan Estimate and your Closing Disclosure Statement, so there should not be any surprises.

Paying close attention to both of these documents prepares you for the amount of cash you’ll need and when.

How to avoid closing costs

There's no way to avoid closing costs entirely, whether you’re buying or refinancing, paying fees at closing or rolling them into your loan. However, there are a few things you can do up front to minimize how much you pay.

Shop for lenders with low fees

Before you decide on a lender, shop around for the best deal. Many of the fees lenders charge are negotiable. Ask each lender for a breakdown of how much they charge in origination fees. You may even want to ask them to break out their bundled origination fees into individual line items. Then compare lenders and negotiate to see which items can be omitted or reduced. A good place to start is with “document prep” or “courier fees.”

Ask the seller to cover some of your closing costs

As a buyer, you can request that the seller pay for some or all of your closing costs while negotiating the offer. Negotiating concessions is common. According to the Zillow Group Consumer Housing Trends Report 2020, 85% of sellers make some kind of trade-off with the buyer to facilitate the sale of a home. This is a beneficial strategy if you don’t have enough cash available after paying your down payment to cover closing costs, too. It’s most commonly used when there are many sellers competing for a small pool of buyers.

Keep in mind that lenders must adhere to regulations that dictate which closing costs sellers can cover for buyers, and the amount sellers can contribute. Be sure to ask your lender about the specifics of your loan program.

Apply for first-time buyer assistance programs

It can be particularly challenging for first-time home buyers to have enough cash to cover both your down payment and closing costs, since you won’t have the proceeds from a previous home sale to use. Luckily, there are numerous assistance programs available for first-timers. And there are some perks available for specific loan types, like VA loans.

Use a no closing cost loan

A no closing cost loan is a bit of a misnomer. It’s more accurate to call it a “no upfront closing cost loan.” Instead of paying your closing costs at closing, this loan type allows you to roll the charges into your total loan amount. The lender may charge you a higher interest rate on the loan for not paying closing costs, or the lender may wrap the closing fees into the total mortgage owed, in which case you’ll end up paying interest on the closing costs.

Mortgage-related closing costs

Many of the closing costs you’ll pay as a buyer are related to the opening of your mortgage. Closing costs can vary significantly based on the type of loan you choose. Here’s a quick summary of what you can expect to pay, based on loan type.

Closing costs on an FHA loan

With an FHA loan, you can expect to pay between 2% and 6% of the home sale price in closing costs. This includes an up-front mortgage insurance premium (MIP) fee paid at closing. (You’ll also make a monthly MIP payment throughout the life of your loan or until you refinance to a conventional loan with 20% equity.)

There are limits on how much of your closing costs the seller can pay on your behalf. It can’t exceed 6% of either the appraised value or the purchase price, whichever is lower.

Closing costs on a conventional loan

Conventional loan closing costs range between 2% and 5% of the purchase price. If you make a down payment of less than 20%, you’ll pay private mortgage insurance until you reach a loan-to-value ratio (LTV) of 78%, when you can request discontinuation of the payment.

Similar to an FHA loan, there are limits to how much of the buyer’s closing costs the seller can cover. If you make a down payment of 25% of the purchase price or more, the seller can pay for closing costs up to 9% of the total loan amount. If your down payment is between 10% and 24%, they can cover up to 6%. For down payments of less than 10%, the seller can assist with closing costs up to a total of 3% of the loan amount.

Closing costs on a VA loan

VA loan closing costs range between 1% and 5% of the total loan amount. The wide range can be attributed to the VA funding fee, which is used in VA loans instead of PMI or MIP. The cost of your funding fee ranges from 0.5% to 3.6% of the total loan cost, depending on a few factors like the type of home you’re buying and if you’ve used VA loan benefits before.

There are limits to seller concessions for VA loans. As the buyer, you can’t have the seller pay more than 4% of the total loan amount in closing costs. Sellers are also not allowed to pay for any loan discount points.

Closing costs on a USDA loan

USDA loan closing costs range from 3% to 6% of the total loan amount. This includes a guarantee fee of 1% of the total loan amount. There is no PMI requirement on USDA loans.

The amount a seller can cover in buyer closing cost is capped at 6% of the home sale price.

What’s included in closing costs?

When you first see your Good Faith Estimate or Closing Disclosure Statement, it can be a little overwhelming — the list of individual line items seems to stretch on and on. Here’s a list of the most common closing costs in alphabetical order, including the general amount of the charge and purpose for the cost.

Application fee

This fee covers the cost for the lender to process your mortgage application. Ask your lender upfront what this fee specifically covers. It may include your credit check or home appraisal, depending on the lender. Not all lenders charge an application fee and you may be able to get it discounted or waived.

Appraisal

Lenders require a home appraisal as part of the underwriting process before approving a mortgage loan. Average appraisals costs range from $300 to $450, and vary in price depending on the location and size of the property. The lender hires an appraiser to provide the fair market value of the home, and the buyer typically pays the lender at closing.

Sometimes a second appraisal fee is charged, called a reinspection fee. This is common when the seller completes repairs on the home that may change the value of the property. A reinspection fee, like the first appraisal, is usually around $300.

Attorney fee

For mortgaged home purchases in many states, an attorney must oversee the closing process. This type of attorney is known as a closing attorney and does not represent the buyer or seller in the transaction. The cost is typically split between the buyer and seller. Settlement costs for using a closing attorney or escrow company to handle the closing of a transaction can range from $500 to $1,500 depending on your location.

Attorneys are required to oversee closing in 21 states and Washington, D.C. These states include Alabama, Connecticut, Delaware, Florida, Georgia, Kansas, Kentucky, Maine, Maryland, Massachusetts, Mississippi, New Hampshire, New Jersey, New York, North Dakota, Pennsylvania, Rhode Island, South Carolina, Vermont, Virginia and West Virginia. In these states, the closing attorney would generally take the place of an escrow company or other settlement agent.

Private real estate attorneys, or borrower’s attorneys, are an additional and optional cost for buyers who want a specialist to assist them with contract-related issues or professional advice beyond the scope of their agent’s abilities. Private real estate attorneys charge by the hour and rates vary based on their level of expertise and services provided.

Credit report fee

Lenders charge a credit report fee of approximately $30. This covers collecting your credit report from all three credit bureaus.

Credit supplement fee

During underwriting, lenders may charge a credit supplement fee to pay credit bureaus to verify that the information on your loan application is up to date, such as your balances and payment histories. This does not occur on all loans during underwriting, but sometimes the initial report occurred in the month prior to closing, and your lender may require a more recent report.

Credit supplement fees are about $15 for each item that requires verification, so the cost to buyers can range from $15 to $100.

Documentation fees

During a financed home purchase, several institutions need to process information and create official records.

Bank processing fee: When banks handle your loan documentation, they’re paid a processing fee, ranging between $25 and $100.

Courier fee: The courier fee allows lenders to quickly send your documents to necessary parties, at a rate of about $20 per courier trip.

Notary fee: A notary makes your signature official. Notaries charge by the signature, about $100 for closing paperwork but they can add fees for their travel.

Recording fee: The lender uses the recording fee (approximately $50) to pay the county to file a public record of the transaction.

Escrow deposit for property taxes and/or mortgage insurance

At closing, buyers are often required to open an ongoing escrow account from which their mortgage servicer will pay ongoing costs. An escrow account is free to open or maintain because it’s a requirement for loans with less than 20% down. If your servicer will be paying your property taxes and/or mortgage insurance on your behalf, you’ll have to start your escrow account with an initial deposit that covers taxes and insurance for the first two months.

Escrow fee or closing fee

This fee is paid to the title company or escrow company that is conducting the closing. Their role is to oversee the transaction as a neutral third party. They also hold funds in an account during the transaction and disperse your down payment, fees and other charges to the appropriate individuals upon closing.

Escrow fees range depending on your location, but are typically about 1% of the home sale price. The cost is typically split evenly between the buyer and seller, but this must be negotiated and detailed in the contract.

FHA up-front mortgage insurance premium (UFMIP)

If you’re using an FHA loan to purchase the home, you’ll be required to pay a premium at closing that totals 1.75% of the base loan amount. You can also roll this into your loan if you’d prefer, but note that you would pay interest on the premium amount.

Flood zone determination fee

This fee is paid to a third-party company that determines if the property is located in a flood zone. It’s an analysis that is often required by lenders. If it is determined that the property is in a flood zone, you will need to buy flood insurance separately.

Home inspection

A home inspection is a common contingency for a home purchase. As the buyer, you can hire an inspector to evaluate the condition of the home and its systems prior to purchase. A home inspection will cost approximately $250 to $700 depending on the size of the property. You will pay the inspector for their service out of pocket, typically at the time of service, not at closing.

Homeowners association transfer fee

When you buy a property that is managed by a homeowners association (HOA), there is typically a transfer fee that covers changing the property owner. During the negotiation, you can detail which party will pay the transfer fee. HOA transfer fees generally cost about $200. At closing, you may also make your first HOA dues payment, prorated based on your closing date.

Homeowners insurance premium

As a stipulation of your financing, you will be required to purchase homeowners insurance. You will continue to pay the insurance premium on a yearly or twice-yearly basis directly to your insurer, or on a monthly basis via an escrow payment that is part of your monthly mortgage payment to your loan servicer. Homeowners insurance policy fees range based on the amount of coverage and the size of the property.

Lender’s policy title insurance

Title insurance is an insurance policy that protects the lender’s interest in the home in case of any problems with the title. It’s similar to a title search, but is paid as its own line item.

Lead-based paint inspection

Some lenders, especially for government-backed loans, require you to have an inspection to ensure the home you’re buying doesn’t have any lead paint. Buyers can also opt to have this inspection done. The buyer is responsible for the cost, which can vary between $250 and $450.

Loan discount points

When locking your interest rate with your lender, you have the option to buy down the rate. To do this, you pay “points” — essentially, paying interest in advance. One point is equal to 1% of the loan; and typically reduces your rate by 0.25%. Not all buyers choose to buy down their interest rate, but if you do, you’ll pay for it at closing.

Mortgage insurance premium

If you finance your home with an FHA loan and pay less than 20% of the price of the home for your down payment, you’ll pay monthly a mortgage insurance premium (MIP). This protects the extra risk your lender is taking on by loaning you more than 80% of the home’s value. You’ll continue to pay this monthly insurance premium for the life of your loan, or until you refinance to a conventional loan with 20% equity (see PMI).

Owner’s policy title insurance

Typically optional for buyers, owner’s title insurance protects you from future claims against the title. The seller typically pays for the owner’s policy, but this needs to be negotiated and detailed in the purchase and sale contract. Owner’s title insurance policies range from $500 to $3,500 depending on the location and size of the property.

Origination fee

Usually one of the largest line items at closing, an origination fee covers the lender’s administrative costs in opening your loan. It’s usually 1% of the total loan amount, but if you shop around, you may be able to find lower fees. Sometimes, lenders offer mortgages with no origination fees.

Pest inspection

Similar to a test for lead paint, a pest inspection inspects the home you’re buying for termites or dry rot. This inspection is required on some government loans and by certain states. While some home inspectors include this service in their standard inspection, many do not. You’ll likely pay a specialty inspection service, and the cost is roughly $100.

Prepaid interest

Because you’ll likely take ownership of your home on a date that’s not the first of the month, you will be responsible for pre-paying any interest that will accrue on your home between the closing date and your first mortgage payment. Your lender will calculate the cost using the daily interest rate, multiplied by the number of days.

Private mortgage insurance (PMI)

If you make a down payment of less than 20% of the purchase price, your lender will require you to pay private mortgage insurance, or PMI, to protect their investment. You may pay a one-time application fee for mortgage insurance at closing. Then, until you’ve reached a set amount of equity in your home (usually 20% or more), you’ll be responsible for making monthly mortgage insurance payments — usually paid by your lender out of your escrow account.

Property taxes

Your property taxes will be prorated based on your closing date. Some buyers pay their taxes in lump sums annually or biannually. If you don’t pay this way, you might escrow the taxes, which means they would be included as an escrow line item in your monthly mortgage payment to your loan servicer.

Survey fee

Some states and lenders require a land survey to be completed for every home purchase. A surveyor will verify all property lines and evaluate things like shared fences. The buyer typically pays this fee, though you may be able to negotiate the cost with the seller. On average, the survey costs around $500, with larger lots costing more.

Title search fee

You’ll pay a title search fee to the title or escrow company, in exchange for doing a thorough search of a property’s public records. This ensures that no one else has a claim to the property you’re buying. The cost is typically less than $100.

Transfer taxes

A transfer tax is a one-time tax or fee imposed by a state, county or local government whenever a property changes hands. It may be a flat fee or a percentage of the home price, and the cost can vary significantly by location.

Underwriting fee

Lenders often charge an underwriting fee, which covers the cost of researching whether or not they should approve you for a loan. Sometimes, this fee is rolled into your origination fee. If it is charged separately, it can range between $400 and $900.

VA funding fee

If you’re using a VA loan to buy your home, you’ll have to pay a VA funding fee at closing. It can cost between 0.5% and 3.6% of the loan amount, depending on the details of your specific purchase. It can be paid at closing or rolled into your total loan amount and paid over time.

Written by

Francesca Faris

05.12.2017

How much home can you afford?

At Zillow Home Loans, we can pre-qualify you in as little as 3 minutes, with no impact to your credit score.

Zillow Home Loans, NMLS # 10287. Equal Housing Lender

Get pre-qualifiedRelated Articles

Thinking about buying but not sure where to begin?

Start with our affordability calculator.

See what you can afford