How will mortgage rates impact seasonal inventory in 2024? Is the seasonal bottom going to happen later than I want? Maybe. It’s not what I wanted to see in 2024, but I have to be realistic since we are already in February.

In the last four years, we have had abnormal seasonal inventory data, meaning that the spring inventory bottom happens later in the year. This is due to demand rising late in one year, pushing through the early part of the next year and preventing inventory growth. Also, when mortgage rates rise, the inventory peak happens later in the year.

I hope we find the seasonal bottom early in February rather than wait for March or April. Since eight of the last nine weeks (excluding the holiday period) have had positive purchase application data, I might need to wait a few more weeks before we see the seasonal bottom.

Weekly housing inventory data

One substantial positive story for 2024 is that we have more housing inventory year over year. It’s not a lot, but anything is positive, which I will take. I am a very pro-housing supply person and will feel much better about the housing market when we return to pre-COVID-19 levels for total active listings. However, last week, inventory fell week to week but was up year over year.

Here is a look at last week:

- Weekly inventory change (Jan. 19-26): Inventory fell from 503,233 to 497,389

- Same week last year (Jan. 20-27): Inventory fell from 466,391 to 457,717

- The inventory bottom for 2022 was 240,194

- The inventory peak for 2023 is 569,898

- For context, active listings for this week in 2015 were 936,253

New listings data

I have been hoping for more new listings data growth in 2024 and even though we’re positive year over year, it’s just not as much as I would like. But at least it’s positive! New listings were trending at the lowest levels ever in 2023, but that should not be the case in 2024. Never forget most sellers are buyers of homes as well, especially if the economy isn’t in a job loss recession. This is a topic I recently discussed on CNBC.

Weekly new listing data for last week over the last several years:

- 2024: 44,167

- 2023: 40,767

- 2022: 40,370

Price cut percentage

Every year, one-third of all homes take a price cut before selling — this is very traditional housing activity. However, when mortgage rates rise and demand gets hit, the price cut percentage data grows year over year.

A perfect example was in 2022: when housing inventory rose faster as demand crashed, the percentage of price cuts rose faster. That increase matched the slope of the inventory increase, and people needed to cut prices to sell their homes. Existing home sales stopped crashing after November of 2022 and this data line has stabilized. As long as this trend continues, we will go below the price cut percentage in 2023 in the spring of this year.

This is the price-cut percentage for the same week over the last few years:

- 2024: 30.6%

- 2023: 33%

- 2022: 19.2 %

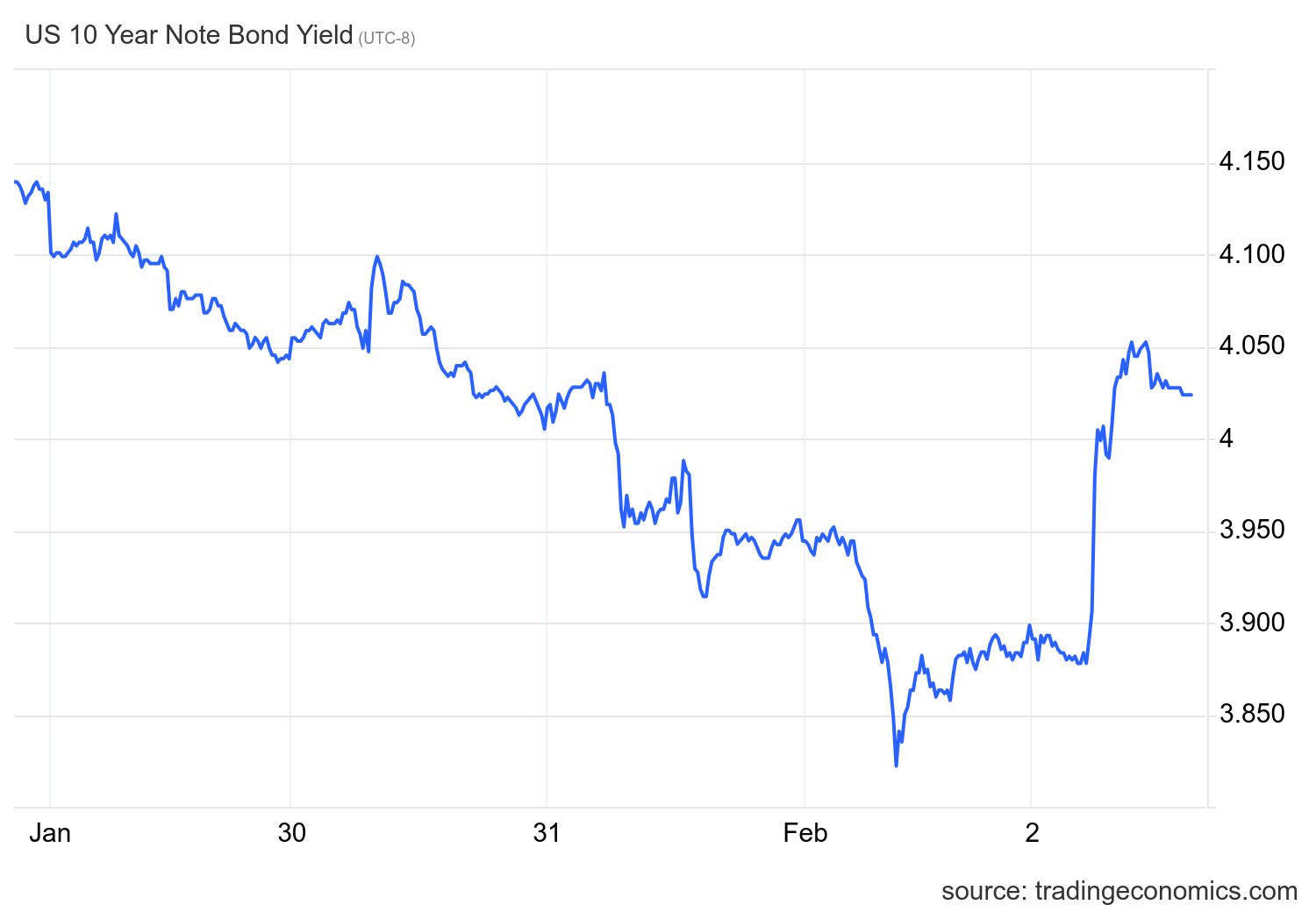

Mortgage rates and the 10-year yield

The 10-year yield is the key for housing in 2024. In my 2024 forecast, I have the 10-year yield range between 3.21%-4.25%, with a critical line in the sand at 3.37%. If the economic data stays firm, we shouldn’t break below 3.21%, but if the labor data gets weaker, that line in the sand — which I call the Gandalf line, as in “you shall not pass” — will be tested.

This 10-year yield range means mortgage rates between 5.75%-7.25%, but this assumes spreads are still bad. The spreads have been improving this year so much that if we hit 4.25% on the 10-year yield, we won’t see 7.25% in mortgage rates.

It was a crazy week for the 10-year yield and mortgage rates as it was jobs week and the Federal Reserve held its Federal Open Markets Committee (FOMC) meeting. The 10-year yield started at 4.13%, got as low as 3.81%, and ended the week at 4.02%. Mortgage rates started the week at 6.88%, fell to a low of 6.63%, then shot up to 6.92% on jobs Friday as the labor data came in stronger than anticipated and the 10-year yield spiked higher with mortgage rates, as you can see in the chart below. I also wrote about the jobs report in this article.

I have always stressed that the labor data is more critical for mortgage rates than the inflation growth rate at this stage. The growth rate of inflation is slowing down noticeably. PCE inflation data is running below 2% on the three- and six-month data line trends, but the 10-year yield is still over 4% and we are near 7% mortgage rates. If jobless claims data ran over 323,000 on the four-week moving average, that would be a different story, as the 10-year yield would be much lower.

Purchase application data

Last week was the first negative week in the purchase application data report since rates fell, as we saw a decline of 11% weekly and they were down 20% year over year. Rates had been ticking up a bit higher, but before last week, it didn’t impact the data much. Eight out of the last nine weeks that I have counted (after making some holiday adjustments) are positive, and for 2024, we have two positive prints versus one negative print.

We always want to weigh this index after the second week of January to the first week of May: After May, total volumes traditionally always fall. Much like 2022-203 data, we have a bounce in demand as mortgage rates have fallen. The question is: how will the rest of the heat months act? Last year, rates spiked up higher and then headed toward 8%. This year should be a different story unless the Fed messes it up.

The week ahead

After a crazy week of labor data and remarks by Fed Chair Jerome Powell, we should have a calmer week with some manufacturing data, household credit data and the all-important jobless claims data.

I will be very interested to see how the 10-year yield trades, especially after Powell talks on 60 Minutes Sunday night — that has the potential to be a market mover. Remember, to their credit, the Federal Reserve used the term restrictive policy when the 10-year yield broke over 4.25% and headed toward 5%. Talk is cheap, and I will need to see some action before they want lower yields to ensure they focus on their dual mandate by keeping prices stable and employment high.