Housing credit channels directly impact housing inventory channels. What does that mean? Home prices escalated out of control after 2020 and when we look at why that happened, we can see that housing credit mattered more to inventory data than most people realize. Let’s see how this has played out in different stages of the economy.

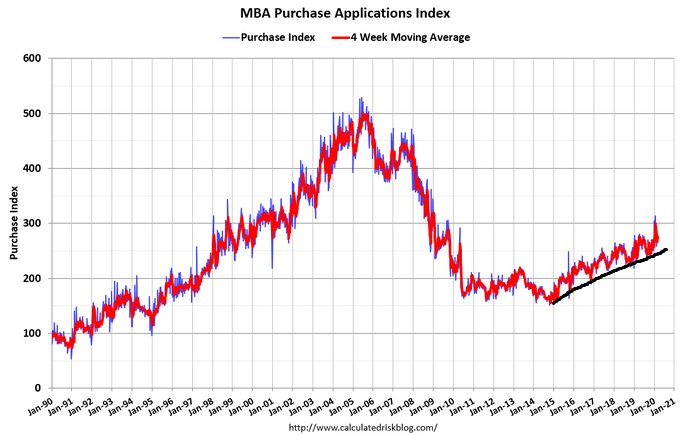

On March 18, 2020, purchase application data broke out to pre-cycle highs in demand. Home sales hit their highest levels in a decade right before COVID-19 hit our economy. This matters because inventory was already heading toward all-time lows before COVID-19.

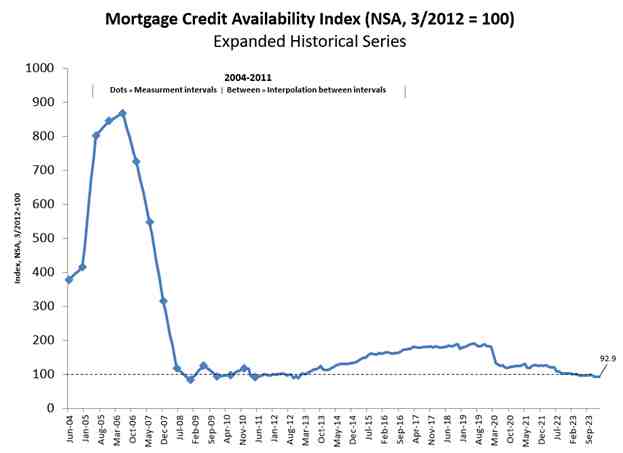

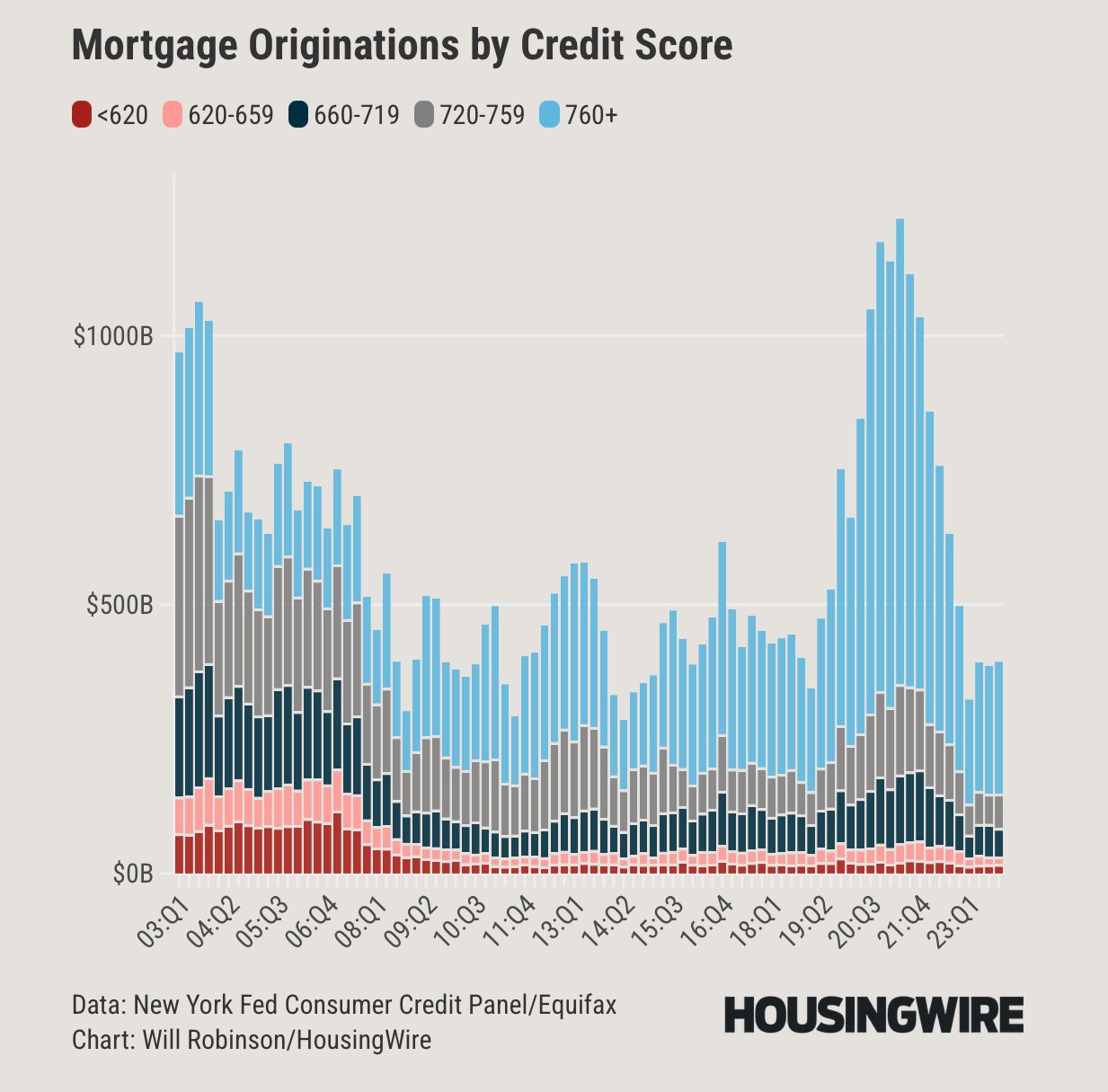

Going back further, the rules put in place after the great financial crisis have had a critical impact on inventory. After 2010, qualified mortgage laws were in place, meaning everyone getting a mortgage has to be able to repay the loan. In practical terms, we no longer have many exotic loan debt structures or the guidelines to allow loose credit. You can see the drastic change this made in the Mortgage Bankers Association Credit Availability index, below, which skyrocketed in 2005 and 2006 before an epic collapse in 2008.

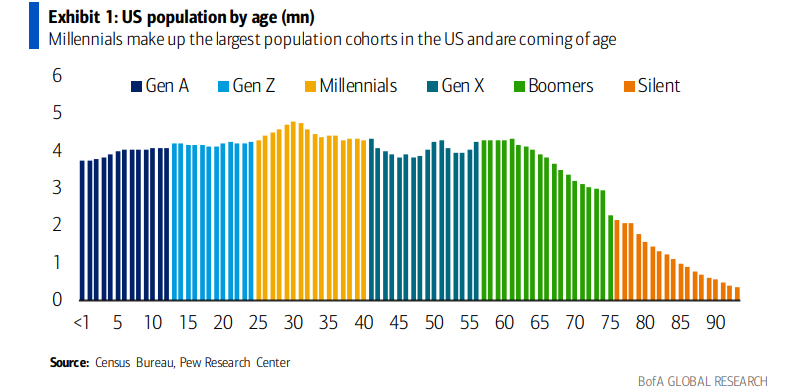

Demographics also play a role here. Since most sellers are buyers, inventory should be stable if demand is stable. However, with first-time homebuyers, they don’t provide a home to sell when they buy, which means they can soak up the inventory. This is what happened post 2010: The millennials started to buy homes in 2013 and they finance 90% of those homes. So inventory slowly broke lower and lower as we came into the years 2020-2024. These years have seen the most enormous housing demographic patch ever recorded in history, with ages 28-35 being massive.

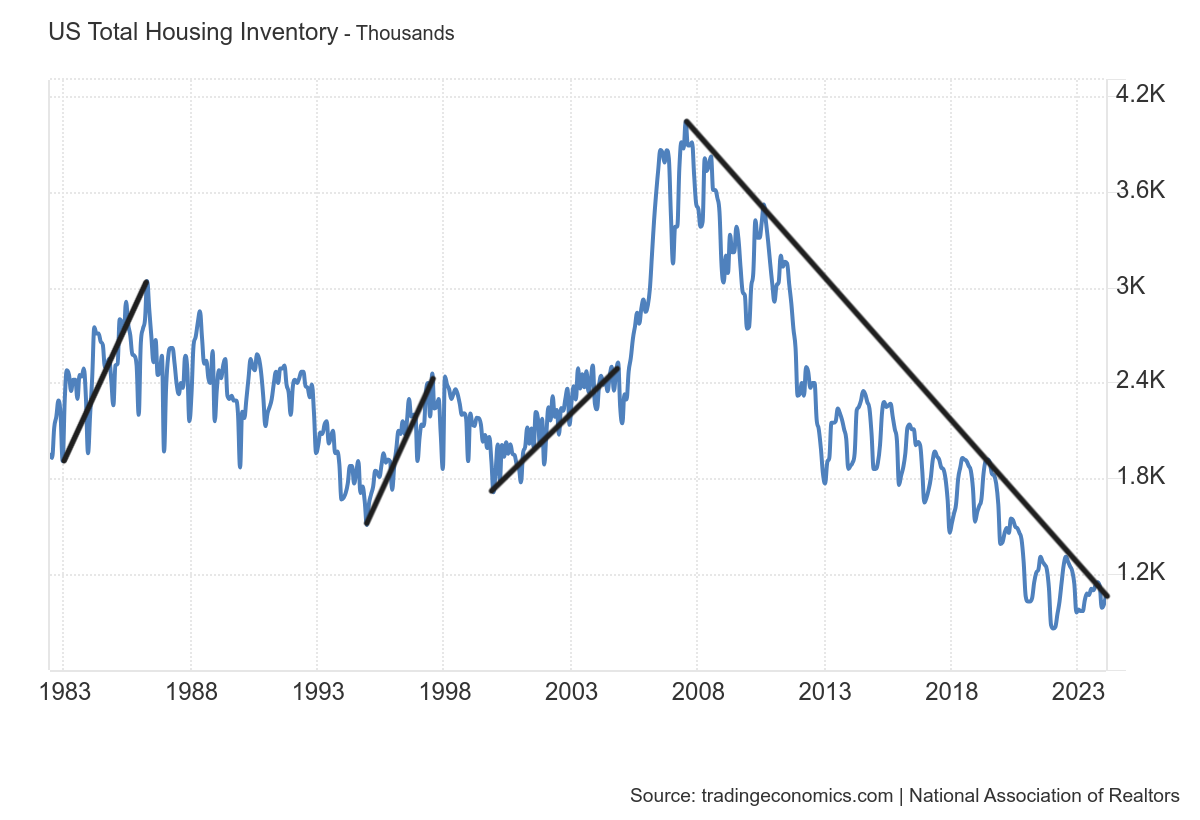

All of these factors set the stage for what happened next. As you can see in the chart below, when we entered 2020, housing inventory was already on the verge of breaking toward all-time lows. In 2022 we had the most significant home sales crash ever and even in 2024 we are in the third year of the lowest number of home sales ever — but inventory is still near all-time lows.

NAR Active Inventory Data, traditionally between 2-2.5 million, currently at 1,110,000

As you can see above, inventory grew at a healthy clip in previous decades and then had a parabolic run higher in 2006 and 2007 when active inventory reached 4 million. So what happened after 2010 that led inventory to these record lows so that even the most significant sales crash in history didn’t move the needle? It comes down to housing credit!

In previous decades, credit flowed more easily and many people could list their homes and buy other homes without the restrictions of the qualified mortgage rule. Now, nobody is listing their homes to sell and buy unless they’re 100% pre-qualified. In the past, when credit was freer, there was no concern about being unable to buy as long as you knew credit was there to assist you.

On top of more legitimate buyers, we fixed the credit markets, meaning housing credit looks fantastic. Just look how lousy credit looked below in 2005, 2006 and 2007 — all before the job-loss recession in 2008. Compare that to how solid credit data looks over the last 13 years since the qualified mortgage laws were implemented.

Americans don’t have a recast rate loan risk; almost all mortgage loans after 2010 are fixed 30-year mortgages, which allows homeowners to benefit from fixed debt costs and rising wages. This means their cash flow is excellent, as the FICO score data has shown us for a long time and they can stay in their houses for as long as they want. So you can see why we have so few stressed sellers.

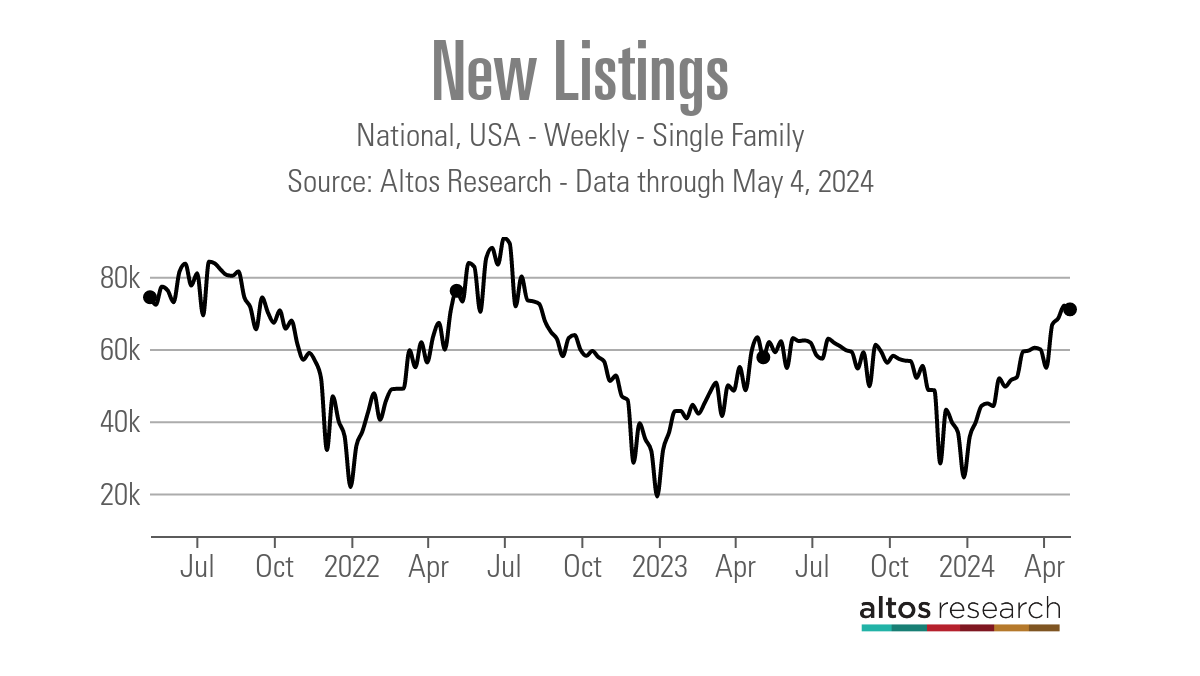

A perfect example is that the last few years, new listings have been trending between 30,000 and 90,000 per week. It didn’t matter if mortgage rates were at 3% or 8%, new listing data has trended at historic lows the past few years. Contrast that to the time from 2008 to 2012 when this data line trended at 250,000 to 400,000 per week. Because credit channels are normal and the quality of homeowners is good, we don’t have a lot of forced selling going on today versus that period.

So when I talk about credit channels running inventory channels, it means housing credit is very boring — and that is a great thing for homeowners and the housing market.

Americans buy a home to live in, raise their kids and go to work; they don’t act like stock traders. With the 30-year fixed mortgage being the staple of the housing credit markets, the inventory data has been trending one way for some time. This doesn’t mean inventory can’t grow in the U.S., but unless we have a job-loss recession, it will take a lot of time to get national inventory levels back to 2019 levels. And those inventory levels weren’t even that high to start with.